Extended Care Planning

Assuring financial security for your

loved ones requires careful planning.

When a loved one experiences an extended care event and needs long-term care, it can impact the entire family. The impact can be felt financially as well as emotionally, and there can be a physical toll too. It’s important to plan ahead in order to protect your family.

What plan have you made? Who will provide the care? Where will the financial resources come from?

As we age, we change in some predictable ways – and in some ways that are completely unexpected. Chronic illnesses or disabilities requiring extended care are rarely planned or anticipated. When it comes to extended care planning, you must ask and answer some

difficult questions in order to provide adequate protection for your loved ones.

You have time to prepare. You have time to protect your family.

A successful extended care plan needs to include an evaluation of your current financial resources and a review of planning options to meet future needs. Because this depends on your personal circumstances, your extended care plan will be unique, and you will need to

determine with your loved ones how best to prepare.

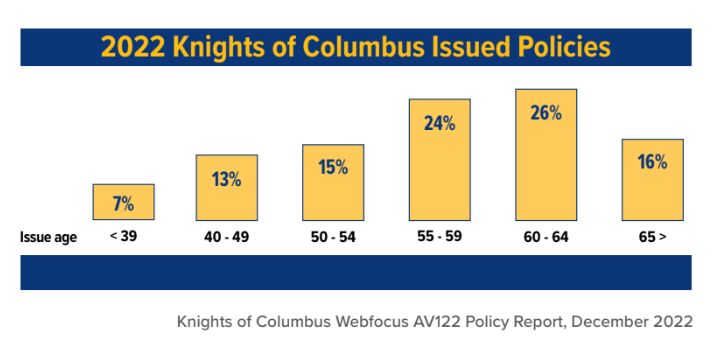

Who BUYS Long-Term Care Insurance?

Long-term care coverage options will be less expensive when you are younger. The likelihood of qualifying for coverage based on underwriting guidelines is also greater at younger ages.

Limited Extended Care Planning

Payment Options

Given these risks and uncertainties, the importance of implementing an extended

care plan becomes clear. There are multiple options to consider.

Government programs offer limited options . . .

Medicare(1)

Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) cover certain medical services and supplies in hospitals, doctors’ offices, and other health care settings. Part A covers: inpatient care in a hospital or skilled nursing facility (not custodial or long-term care), hospice, home health care and inpatient care in a religious nonmedical health care institution. Part B covers medically necessary doctors’ services.

Medicaid(2)

Medicaid can pay for most long-term care services if you are eligible after your assets fall below a certain level. This joint federal and state program determines eligibility based on countable assets that must be below allowable amounts.

The default option without a plan is . . .

Self-Funding

Self-funding means that the income to pay for your long-term care event must come from your savings or other assets. What was the original purpose of your savings account? What role does your current investment portfolio play in your financial future? Were either of these created in order to pay for an extended care event?

The best planning option for you and your family is . . .

Long-Term Care Insurance

Long-term care insurance is expressly designed to pay for an extended care event. It is an important element of your overall financial plan. Depending upon the type of long-term care policy that you choose for your individual plan, you can receive benefits whether you are being cared for in your home or in a facility. More importantly, your family will have a viable plan to address your needs.

(1) Medicare+You 2019, Department of Health+Human Services, (Pages 5,6 and7), www.medicare.gov

(2) Paying for Senior Care, Medicaid and Long-Term Care for the Elderly(Updated-June 2018), ww.payingforseniorcare.com/longtermcare/resouces/Medicaid.html

Government programs offer limited options . . .

Medicare(1)

Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) cover certain medical services and supplies in hospitals, doctors’ offices, and other health care settings. Part A covers: inpatient care in a hospital or skilled nursing facility (not custodial or long-term care), hospice, home health care and inpatient care in a religious nonmedical health care institution. Part B covers medically necessary doctors’ services.

Medicaid(2)

Medicaid can pay for most long-term care services if you are eligible after your assets fall below a certain level. This joint federal and state program determines eligibility based on countable assets that must be below allowable amounts.

The default option without a plan is . . .

Self-Funding

Self-funding means that the income to pay for your long-term care event must come from your savings or other assets. What was the original purpose of your savings account? What role does your current investment portfolio play in your financial future? Were either of these created in order to pay for an extended care event?

The best planning option for you and your family is . . .

Long-Term Care Insurance

Long-term care insurance is expressly designed to pay for an extended care event. It is an important element of your overall financial plan. Depending upon the type of long-term care policy that you choose for your individual plan, you can receive benefits whether you are being cared for in your home or in a facility. More importantly, your family will have a viable plan to address your needs.

(1) Medicare+You 2019, Department of Health+Human Services, (Pages 5,6 and7), www.medicare.gov

(2) Paying for Senior Care, Medicaid and Long-Term Care for the Elderly(Updated-June 2018), ww.payingforseniorcare.com/longtermcare/resouces/Medicaid.html

Protect What Matters Most.

Your Life. Your Family. Your Future.

In 1882, Father Michael J. McGivney founded the Knights of Columbus as an organization

to provide for the financial security of Catholic families. Since that time, the Order has grown to

include life insurance, disability income insurance, long-term care insurance, and retirement annuities.

Meet with your field agent today and join the many other Catholic families that are insured

with Knights of Columbus.

To learn more about our

Fraternal Benefits and to join the

Knights of Columbus, visit

Contact Us

You can unsubscribe from these communications at any time. For more information on how to unsubscribe, our privacy practices, and how we are committed to protection and respecting your privacy, please review our Privacy Policy. By clicking submit below, you consent to allow Stackowicz Agency to store and process the personal information submitted above to provide you the content requested.